This is the time of year when many people make an effort to get a handle on their budget. People are turning their thoughts to self-improvement and personal finance is on their minds.

This is the time of year when many people make an effort to get a handle on their budget. People are turning their thoughts to self-improvement and personal finance is on their minds.

Generally speaking the ability to save money monthly depends on what you do everyday. Do you ask yourself each day if you are adding or subtracting to your net worth?

Companies like Wallet.ai are developing algorithms that will help you answer these questions and send you a notification when you are getting off the savings path. They will analyze your spending patterns and then send you text messages suggesting ways you can cut back. Someday we may be turning over our financial control to a robot.

Until that day comes, people still need to rely on good common sense while doing their financial planning. Below, you will find some helpful money saving tips to use in 2014.

1. Lower Media Consumption

Look into all the media that you are consuming on a daily basis. That means your cell phone, your home internet access, your cable television, your extra devices, like iPads or tablets and add them all up. The bill can easily add up to over $300 a month. Talk to your providers and see about how you can reduce this amount and still enjoy the media that is most important to you.

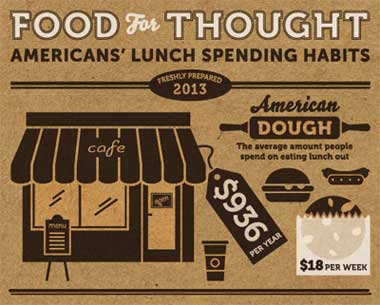

2. Spend Less On Dining Out

Let’s face it, dining out is enjoyable and like it or not, you will make all kinds of exceptions in your head about why you need to eat out. To combat this, try hitting restaurants that have happy hours and dinner entrees at half price. Check the coupon sites for restaurant specials. Forgo the expensive dessert, fancy waters and cocktails. When reading your menu, don’t ignore prices just because there is no dollar sign in front of the numbers.

3. Spend Less On Movies

Going out to the movies will always be a powerful form of entertainment. Ticket prices have gone up in some theaters to $11.50 per person. Watch for special days that theaters reduce their prices and you can sometimes save up to 50% off. If you have Netflix at home, watching episodes of good television productions has become so popular that newscasters have coined a new phrase for 2013 – “Binge Watching.” You may get caught up in this activity for days at a time, but still you will be saving entertainment money by staying at home.

4. Enjoy Nature

The outdoors provides plenty of opportunities for enjoyment. Hiking local trails will keep you away from shopping centers and provide you with good exercise as well. If you are trapped inside because of bad weather, try your local indoor gyms.

5. YouTube Parties

Gather your friends together and have everybody contribute their favorite “funniest YouTube videos.” Television producers aren’t the only ones that can provide you entertainment.

6. Cut Back Cruising Expenses

Save money by bringing your own wine on board and by booking spa treatments ahead of time. Arrange to be a guest speaker on board the ship to lower costs. Book an inside room instead of a room with an ocean view. You’ll have plenty of time to have enjoy the ocean. Check for deals at VacationsToGo.com.

7. Read More

If you are looking for action and adventure, BuzzFeed published reviews of 16 books they judge as perfect movie scripts. Make your reading more enjoyable by using a Kindle PaperWhite which holds over 1,000 books and is small enough to easily carry around with you. With free 3g connections in over 100 countries, no contracts and no monthly fees, reading has never been more convenient.

8. Save 10% or More Of Your Income

When people tell you to pay yourself first, they mean save part of your income. Decide on a percentage to save each month and then set up an automatic transfer to your savings account so that it is done automatically. This system of automatic transfers makes savings much easier.

9. Avoid Buying Just Because It’s ON SALE

Everyone uses different criteria for spending, but one common problem is that people see things on SALE and make purchases just because of the sale. There isn’t anything wrong with doing that if the purchase is within your budget. The question that fails to get asked is “Do I Really Need This Item?”

10. Avoid Thinking “There is room on my credit card.”

Silly as this may sound, some people decide they can afford something if they have room on their credit card for it. Of all erroneous purchasing strategies, this is the worst one to make. You should be paying off your credit card expenses every month. You should also remember that there is a rule about the amount of credit that is extended to you. Credit scores are based on the percentage of debt extended to you and the balance you owe. Best advice is to keep this under a 50% ratio to maintain good credit scores.

We look forward to hearing what your best money saving strategies are in 2014. Please let us know by commenting below.