You might opt to buy a share of stock in the largest business in the country, then the second largest, etc., down the line. You’d have used up the $1,000 before you got to the 20th stock, according to etrade.com.

Another option would be to buy a mutual fund. That would open the option to spread your $1,000 among a great choice of stocks and bonds. If you invest through an Individual Retirement Account (IRA) you might get launched for less than $1,000. Some funds are available for as little as $50 per month if you are willing to make an ongoing commitment. Mutual Fund managers invest your money in a wide variety of stocks giving you a better chance to have your investment grow over time.

Mutual funds are easy to buy, whether you are going it alone or hire a broker or financial planner to do the job. Once you are established with a fund company, a simple phone call or mouse click can initiate a purchase, although there are some “closed funds,” which will not accept money from new shareholders.

Selling also is easy. When you are ready to unload shares, you don’t have to find a buyer. Most mutual funds offer daily redemptions, so the company will give you your cash whenever you’re ready to sell. If you own closed funds, you also can sell when you choose.

You don’t have to worry about the safety of your investment if you turn your business over to a manager. The Investment Company Act of 1940, following close on the heels of the Great Depression, is the federal government’s way of safeguarding your money. Mutual funds are regulated by the Securities and Exchange Commission. You become an owner of the company, which must have a board of directors to protect member investors. Their job is to ensure that the company has the best possible managers and that shareholders aren’t overpaying for their services.

That’s good, but not foolproof. Mutual funds are not insured or guaranteed. You can lose money because your portfolio is based on all of its holdings. If they lose value, you will lose money. The odds of losing all your money, however, are slim. All of the stocks and bonds in your portfolio would have to lose value entirely for that to happen. Historically, the funds have done well.

Though you need some savvy to do effective investing, you don’t need to know how to read a company’s cash flow statement or be able to predict whether it might fail to meet debt obligations. You pay a fund manager to make those judgments and put your money where it will produce a return. Mutual funds are not assured and are subject to market vagaries like other investments, but they are a good choice for people who don’t have the money, time or interest to gather a collection of securities by themselves.

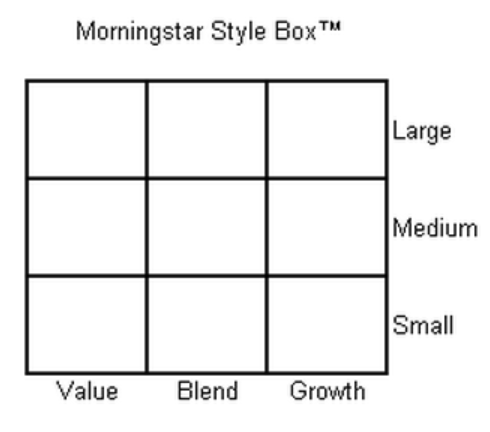

(Information copyrighted by Morningstar, Inc, All rights reserved.)

This configuration allows you to place your chosen fund its correct category (one box on the “tic tac toe” spectrum). This is helpful because it will allow you to compare total performance (rates of return) with funds of a similar size and investment approach. Typically, investors make these comparisons over 3, 5, and 10 year time horizons (allowing you to smooth out short term fluctuations in the market). Of course, performance comparisons can also be made relative to a benchmark index like the S&P 500, but the more specific performance comparisons (to those funds in a similar Morningstar category) tend to be more useful.

This configuration allows you to place your chosen fund its correct category (one box on the “tic tac toe” spectrum). This is helpful because it will allow you to compare total performance (rates of return) with funds of a similar size and investment approach. Typically, investors make these comparisons over 3, 5, and 10 year time horizons (allowing you to smooth out short term fluctuations in the market). Of course, performance comparisons can also be made relative to a benchmark index like the S&P 500, but the more specific performance comparisons (to those funds in a similar Morningstar category) tend to be more useful.